I’ve been meaning to talk about this article for months, because it infuriates me. I spent a total of 22 years working in the banking industry: 14 at a big six bank, and 8 more at a smaller challenger bank (which railed against the kind of stuff described below). Based on what I saw working at that big bank, nothing in this article surprises me.

From the CBC:

Marketplace has spoken confidentially to current and former bank employees from all the big banks: TD, RBC, BMO, Scotiabank and CIBC. CBC is concealing their identities because they fear professional repercussions. All expressed similar concerns about enormous sales pressure they say leads to potentially costly or otherwise dangerous financial products being pushed on customers.

“I had to mislead customers into getting products that they didn’t need, to reach my sales target,” said a recent BMO employee.

“It’s not a customer service … environment,” a former Scotiabank employee said. “We’re there to sell — and make money for the bank.”

While I never worked in a branch, it was common knowledge that this happened. Branch staff had monthly sales quotas. I personally witnessed — as a customer long after I left that bank, mind you, not as an employee — staff in a different big six bank offering products to a customer that they obviously did not need, not because they wanted to, but because the system prompted them to and they knew they’d be in trouble if they didn’t ask.

They will push credit products and other revenue-generating products in order to meet sales quotas, vs. giving advice which would benefit the customer. From the same article:

In a second test, Marketplace sent a colleague wearing hidden cameras to meet with financial advisors at the big five banks.

She posed as a customer with a $50,000 inheritance coming soon and wanted financial advice. If asked, she said she also had a $350,000 mortgage and $17,000 in credit card debt.

None of the advisors asked about existing debt, instead recommending that our tester invest the full $50,000 in products like GICs and mutual funds, which help bank employees hit their sales targets.

When our tester raised the credit card debt herself, only BMO and CIBC clearly recommended that she use part of the supposed inheritance to pay it off in full.

Anyone with a basic knowledge of budgeting and money management would tell you to pay down high-interest debt before investing. But they get away with this predatory bullshit because customers assume that bank branch employees have a fiduciary duty to help them. THEY 👏 DO 👏 NOT 👏.

In one recording, a manager tells Jeraline that in order to make more sales, she should remember that she does not work in customer service.

“We are investment advisors,” he says. “You have to have a bit of aggression.”

Unlike registered financial advisers, financial advisors (spelled with an “o”) at banks have no fiduciary requirement to their customers.

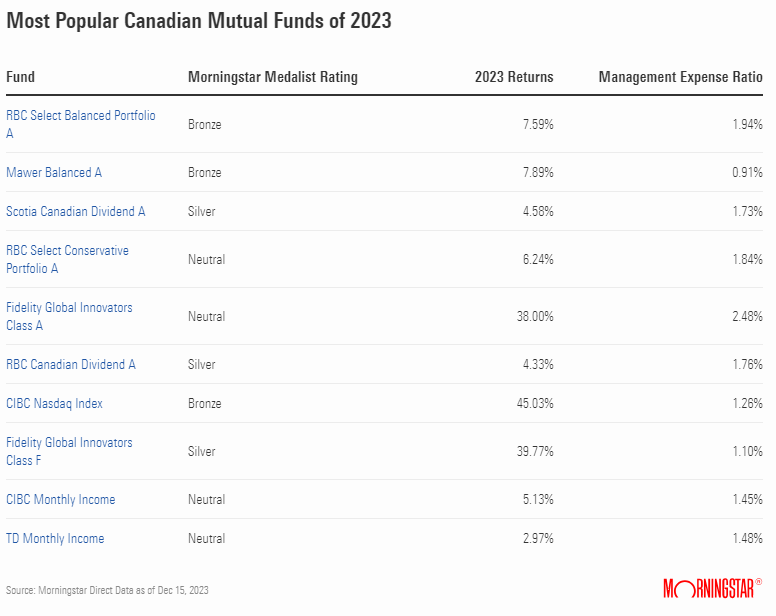

I say this to everyone who tells me about their investments at their bank. 9 times out of 10 it’s some mediocre bank-owned mutual fund which was recommended not because it’s the best option for the customer, but because it makes the bank the most money. Look at this list of the largest mutual funds in Canada, or this table from Morningstar.ca showing the most popular funds on their site last year.

7 of those 10 funds are from big banks, despite their largely mediocre performance. In fact, by the time you subtract the MER, 4 of those 7 big bank mutual funds earned less last year than my everyday bank account. The only reason these funds grew so big is because bank staff recommend them regardless of their performance or suitability to the customer.

Most people are surprised when I tell them the bank employee who sold them a high-fee mutual fund owes them no fiduciary duty. They shouldn’t be. Those banks are designed to maximize their own profits at the expense of their customers, in spite of their spokespeople’s protestations or what their multimillion-dollar marketing campaigns tell you. I didn’t see that — or didn’t want to see it — until I stopped working at one…and I have a Commerce degree and an MBA, plus decades of hands-on experience. My heart breaks for the people who get taken advantage of day in and day out by a predatory oligopoly.